Micro, Small, and Medium Enterprises (MSMEs) are the heartbeat of India’s economy, contributing nearly 30% to the country’s GDP and employing over 110 million people. Whether it’s a small textile manufacturer in Surat, a local bakery in Bengaluru, or a budding tech startup in Pune, MSMEs fuel innovation, create jobs, and drive regional development.

To simplify this, the government introduced Udyog Aadhaar, and, in 2020, transitioned to Udyam Registration—a move designed to make life easier for MSMEs.

For many small business owners, dealing with paperwork and compliance can feel overwhelming. Udyam Registration streamlines the process, making it easier to access financial aid and government schemes and even improving business credibility.

Table of Contents

What is Udyog Aadhaar?

Udyog Aadhaar was introduced as a unique identification number for MSMEs to simplify the registration process. It replaced the older Small Scale Industries (SSI) registration system, allowing businesses to register with just a single-page form.

The primary purpose of Udyog Aadhaar was to ease the bureaucratic burden on small businesses and provide them with access to government schemes, subsidies, and financial assistance. This simplified registration made it easier for MSMEs to establish credibility and seek funding opportunities.

What is Udyam Registration?

Udyam Registration is the updated and more comprehensive registration system for MSMEs under the Ministry of Micro, Small, and Medium Enterprises.

Unlike Udyog Aadhaar, Udyam Registration is mandatory for businesses to avail themselves of government benefits after 2020. The online registration allows businesses to self-certify their classification as micro, small, or medium enterprises.

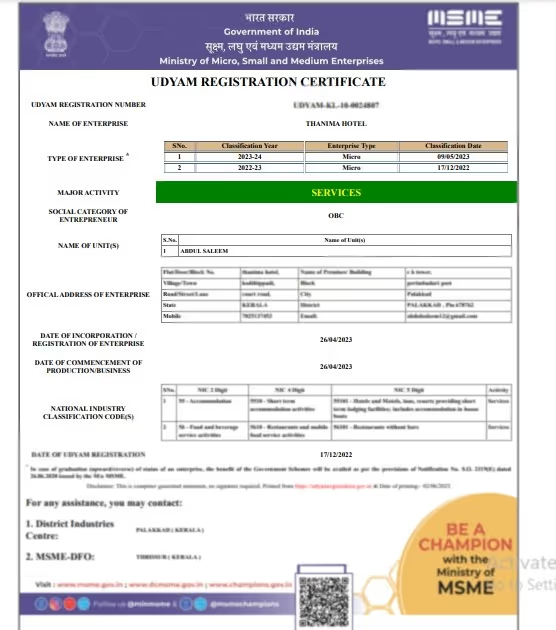

The Udyam Registration Certificate is an official document issued by the Ministry of Micro, Small, and Medium Enterprises (MSME) to businesses that successfully register under the Udyam portal. This certificate serves as legal proof of a business’s MSME status and contains a unique Udyam Registration Number.

Since the entire process is online and paperless, businesses can obtain their Udyam Registration Certificate quickly, ensuring seamless access to financial aid and growth opportunities.

Difference Between Udyog Aadhaar and Udyam Registration

Here is the difference between Udyog Aadhaar and Udyam Registration:

{{pvt-cta}}

Top 5 Benefits of Udyog Aadhaar

1. Access to Government Schemes and Subsidies

- Udyog Aadhaar holders could apply for various MSME support programs, including credit-linked subsidies and financial aid.

2. Easier Loan Approvals

- Banks and financial institutions provided loans at lower interest rates to Udyog Aadhaar-registered businesses.

3. Enhanced Business Credibility

- Registration helped businesses gain recognition and build trust with customers, investors, and suppliers.

4. Simplified Government Tender Applications

- Businesses could easily apply for government tenders, increasing their opportunities in public sector projects.

5. Tax Rebates and Concessions

- Udyog Aadhaar allowed businesses to benefit from various tax exemptions, reducing operational costs.

5 Key Benefits of Udyam Registration

1. Official Recognition and Credibility

- Udyam Registration serves as proof of a business’s legal status, making it easier to secure partnerships and attract investors.

2. Better Financial Support

- MSMEs registered under Udyam get easier access to bank loans, credit facilities, and government funding programs.

3. Simplified Access to Government Schemes

- Registered businesses can avail themselves of subsidies, grants, and financial incentives tailored for MSMEs.

4. Tax Benefits

- Udyam-registered MSMEs enjoy tax rebates and exemptions, reducing their overall financial burden.

5. Priority Access to Government Contracts

- Udyam Registration ensures that businesses get priority consideration in public sector tenders, helping them grow through government contracts.

How to Migrate to Udyam Registration?

With Udyam Registration now mandatory for government benefits, MSMEs registered under Udyog Aadhaar must migrate to the new system. The migration process is straightforward:

- Visit the Udyam Registration Portal

- Go to the official Udyam Registration website.

- Enter Udyog Aadhaar Details

- Provide your Udyog Aadhaar number along with Aadhaar-linked mobile details.

- Submit PAN and GSTIN

- Enter PAN and GSTIN details for verification.

- Complete Self-Declaration

- Fill in business classification details based on investment and turnover.

- Receive Udyam Registration Certificate

- After successful verification, the Udyam Registration certificate is generated.

Migrating to Udyam Registration ensures businesses continue to enjoy financial aid, easier access to credit, and government compliance.

Register Your Limited Liability Company With Razorpay Rize now at just Rs. 1499*!

Conclusion

Understanding the differences between Udyog Aadhaar and Udyam Registration is essential for MSMEs to stay compliant and competitive.

While Udyog Aadhaar served as a stepping stone for MSMEs, Udyam Registration is now mandatory for accessing government benefits, funding opportunities, and enhanced business credibility.

Migrating to Udyam Registration ensures businesses remain eligible for financial support and government schemes, enabling them to grow and thrive in India’s evolving economic landscape. If you haven't yet migrated, now is the time to secure your business's future with Udyam Registration!

Frequently Asked Questions

Private Limited Company

(Pvt. Ltd.)

- Service-based businesses

- Businesses looking to issue shares

- Businesses seeking investment through equity-based funding

Limited Liability Partnership

(LLP)

- Professional services

- Firms seeking any capital contribution from Partners

- Firms sharing resources with limited liability

One Person Company

(OPC)

- Freelancers, Small-scale businesses

- Businesses looking for minimal compliance

- Businesses looking for single-ownership

Private Limited Company

(Pvt. Ltd.)

- Service-based businesses

- Businesses looking to issue shares

- Businesses seeking investment through equity-based funding

One Person Company

(OPC)

- Freelancers, Small-scale businesses

- Businesses looking for minimal compliance

- Businesses looking for single-ownership

Private Limited Company

(Pvt. Ltd.)

- Service-based businesses

- Businesses looking to issue shares

- Businesses seeking investment through equity-based funding

Limited Liability Partnership

(LLP)

- Professional services

- Firms seeking any capital contribution from Partners

- Firms sharing resources with limited liability

Frequently Asked Questions

What is the difference between Udyam and Udyog Aadhaar?

Udyog Aadhaar was the earlier system for MSME registration, while Udyam Registration replaced it in 2020 to make the process more streamlined and mandatory for availing government benefits. Udyam requires additional details like PAN and GSTIN and provides better government support.

Is it mandatory to convert Udyog Aadhaar to Udyam?

Yes, businesses that were previously registered under Udyog Aadhaar must migrate to Udyam Registration to continue availing of government schemes, subsidies, and benefits.

Can I have two Udyam registrations?

No, an enterprise can have only one Udyam Registration linked to its PAN. However, a business can list multiple activities under the same registration.

How long does it take to get a Udyam number?

After obtaining Udyam Registration, businesses should:

What is the next step after Udyam registration?

After obtaining Udyam Registration, businesses should:

- Download the Udyam Certificate for records.

- Apply for government schemes and financial support.

- Update business details if required.

- Utilise benefits such as loans, tax exemptions, and subsidies.

Who is eligible for Udyam?

Micro, Small, and Medium Enterprises (MSMEs) engaged in manufacturing, production, processing, or service activities are eligible for Udyam Registration. The eligibility is based on turnover and investment limits defined by the government.

Who is eligible for Udyog Aadhaar?

Previously, Micro and Small Enterprises could register under Udyog Aadhaar. However, this system has been replaced by Udyam Registration, which is now the mandatory process.

Is Udyog Aadhaar free of cost?

Yes, Udyog Aadhaar registration was free of cost. Similarly, Udyam Registration is also completely free and can be done online through the official MSME portal.

.png)

Akash Goel is an experienced Company Secretary specializing in startup compliance and advisory across India. He has worked with numerous early and growth-stage startups, supporting them through critical funding rounds involving top VCs like Matrix Partners, India Quotient, Shunwei, KStart, VH Capital, SAIF Partners, and Pravega Ventures.

His expertise spans Secretarial compliance, IPR, FEMA, valuation, and due diligence, helping founders understand how startups operate and the complexities of legal regulations.